This post includes an excerpt of the research in the February/March/April edition of Wood Bioenergy US (WBUS) and is the first part of a two part series on liquid biofuels.

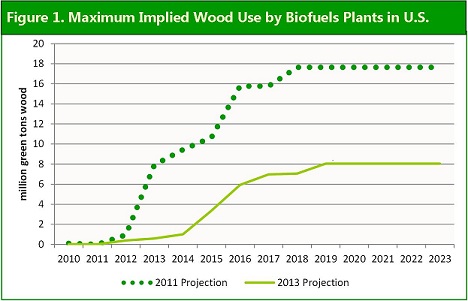

In May 2011, Forisk and the Schiamberg Group evaluated the viability of 36 wood biofuel projects in the United States. The study emphasized the unlikely and problematic development of the wood biofuels sector while singling out projects with drop-in fuels and specific technology types as having investment potential for investors. As of April 2013, 13 of the original 36 projects have been cancelled and 12 remain in the planning or construction stages. Four have been shut down. Since the 2011 study, ten new wood biofuel projects have been announced. New projects emphasize feedstock flexibility beyond wood raw materials and focus on multiple, existing end markets including diesel, sugars and industrial chemicals. Analysis of potential wood use highlights the minimal relevance of the biofuels projects to timberland investors in the U.S. today and over the next ten years (Figure 1).

Newly announced wood biofuel projects have become increasingly less ambitious and less relevant to forest industry firms and timberland investors. Analysis comparing projects in 2013 to those from 2011 find that current projects use less wood and scale at smaller production levels. Meanwhile, the traditional forest products industry is reopening closed plants and building new capacity in response to increasing housing demand.

In the bioenergy sector, wood pellets provide a ready, realizable market. The enthusiasm for wood biofuels from a few years ago has been replaced with well-earned skepticism and caution. For timberland investors, potential demand and wood-based revenues from biofuels have been discounted. For traditional forest industry firms, biofuel worries have been replaced by demands to be treated fairly in legislation or mandates that could affect wood raw material costs. And for biofuel investors and project developers, the needs to produce product for existing markets that can produce cash today have strengthened business models and modified expectations for potential growth in the next five years.

WBUS Market Update: As of April 2013, WBUS counts 456 announced and operating wood bioenergy projects in the U.S. with total, potential wood use of 125.0 million tons per year by 2023. Based on Forisk analysis, 293 projects representing potential wood use of 75.4 million tons per year pass basic viability screening. To download the free WBUS summary, click here.